Backstage & Influences

There are some exceptions to this rule, but always apply the cost principle unless FASB has specifically stated that a different valuation method should be used in a given circumstance. The conceptual framework sets the basis for accounting standards set by rule-making bodies statement of retained earnings example that govern how the financial statements are prepared. Here are a few of the principles, assumptions, and concepts that provide guidance in developing GAAP. Some companies that operate on a global scale may be able to report their financial statements using IFRS.

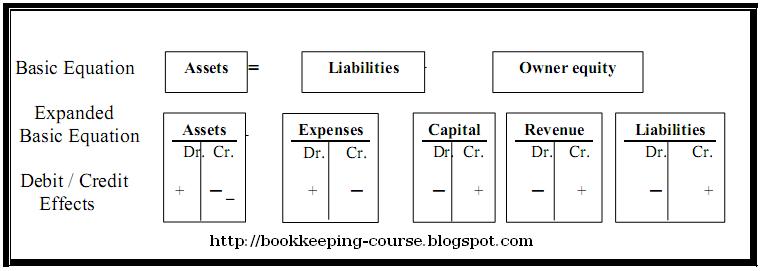

Accounting Equation

These include patents, copyrights, trademarks, and other rights. The preparation of the financial statements is the summarizing phase of accounting.

For example, a company’s pension plan obligations will change as more employees retire, but it will never be a current liability. The length of time that your company has held the asset isn’t relevant on a balance sheet.

What is a balance sheet example?

Yes, Cash is a real account. It is an item of Current Assets and it is carried forward to the next year unlike nominal accounts which are closed at the end of the year. It is an asset and so it a real a/c. Examples of tangible real accounts are land, building, machinery, cash, etc.

As a result, financial statement users are more informed when making decisions. The SEC not only enforces the accounting rules but also delegates the process of setting standards for US GAAP to the FASB. Recalculate the retained earnings balance and make sure it uses the right data from the general ledger. However, there are more ways to troubleshoot your balance sheet.

Your statement of retained earnings and financial planning

It’s more important to think about what your company can do with that asset in the future. It’s possible that the first assets listed will be some adjusting entries of your company’s smallest. Intangible assets refer to non-monetary assets that have no physical substance and will last more than 1 year.

For example, Lynn Sanders purchases a piece of equipment for $40,000. She believes this is a bargain and perceives the value to be more at $60,000 in the current market. Even though Lynn feels the equipment is worth $60,000, she may only record the cost she paid for the equipment of $40,000. The primary exceptions to this historical cost treatment, at this time, are financial instruments, such as stocks and bonds, which might be recorded at their fair market value.

What are basic accounting terms?

Generally accepted accounting principles, or GAAP, are a set of rules that encompass the details, complexities, and legalities of business and corporate accounting. The Financial Accounting Standards Board (FASB) uses GAAP as the foundation for its comprehensive set of approved accounting methods and practices.

The preparation of the financial statements is the seventh step in the 9-step accounting cycle. We will take a look at them first before getting into the whole process for you to have a http://bountifulyou.com.au/2020/03/02/discovering-the-4-types-of-accounting-2/ picture of what we are trying to produce in an accounting system. Numbers are the foundation of any business — and no one knows numbers better than accounting and finance professionals.

But to succeed as a financial professional in today’s competitive landscape, you need more than numerical know-how; you need the expertise to conduct analysis and leverage data to drive business decisions. That’s exactly what the online Master of Accountancy from Ohio University prepares you to do.

- Thecash flow statementshows the amount of cash and cash equivalents entering and leaving a company.

- Income accounts move equity positively, so Credit increases Income accounts.

- This transaction is recorded as an increase in the asset « gas » for $5, and a corresponding reduction in the asset « cash » for $5.

just simple question .wat are the three golden rules of accounts?

Multiple types of accounting careers exist within the financial industry, with each performing a differing range of functions. Branches of accounting vary based on the employment setting, range of responsibilities and daily activities, types of available advancement, and other factors. This article will break down various types of accounting and their careers into four broad categories. Though different professional accounting sources may divide accounting careers into different categories, the four types listed here reflect the accounting roles commonly available throughout the profession. These four branches include corporate, public, government, and forensic accounting.

An undergraduate degree is most often required for any accounting career, while previous master’s work, especially in the accounting field, is often strongly preferred. Below, we’ll explore the nuances of each common area of accounting. These accounts are related to individuals, firms, companies, etc.

Equity consists of contributed capital (money invested) and retained earnings (historical sum of profits and losses). Here, make a list of all the equity accounts like common stock, treasury stock, and the retained earnings number from Step 1. Current liabilities include debts that the company must pay off within the next year. Fixed liabilities, such as mortgages, are considered long-term debts because they will not be settled this year. The company’s debts will fluctuate over time, but this does not affect whether they are considered current or fixed liabilities.

ACCOUNTING

These principles are used in every step of the accounting process for the proper representation of the financial position of the business. Accounting principles are essential rules and concepts that govern the field of accounting, and guides the accounting process should record, analyze, verify and report the financial position of the business. Once all of the claims by outside companies and claims by shareholders are added up, they will always equal the total company assets. It’s also an important statement lenders use when determining whether you can borrow money.

A few examples of personal accounts include debtors, creditors, banks, outstanding/prepaid accounts, accounts of credit customers, accounts of goods suppliers, capital, drawings, etc. All assets of a firm, which are tangible or intangible, fall under the category “Real Accounts“. This concept is basically an accrual concept since it disregards the timing and the amount of actual cash inflow or cash outflow and concentrates on the occurrence (i.e. accrual) of revenue and expenses. It is wrong to recognize revenue on all sales, but charge expenses only on such sales as are collected in cash till that period.

, states that virtually everything the company owns or controls (assets) must be recorded at its value at the date of acquisition. For most assets, this value is easy to determine as it is the price agreed to when buying the asset from the vendor.

Real Accounts

prescribes that a business may only report activities on financial statements that are specifically related to company operations, not those activities that affect the owner personally. This concept is called the separate entity concept basic accounting equation because the business is considered an entity separate and apart from its owner(s). Once an asset is recorded on the books, the value of that asset must remain at its historical cost, even if its value in the market changes.

The SEC regulates the financial reporting of companies selling their shares in the United States, whether US GAAP or IFRS are used. The basics of accounting discussed in this chapter are the same under either set of guidelines. You also learned that the SEC is an independent federal adjusting entries agency that is charged with protecting the interests of investors, regulating stock markets, and ensuring companies adhere to GAAP requirements. By having proper accounting standards such as US GAAP or IFRS, information presented publicly is considered comparable and reliable.

For example, a business might have certain expenses that are paid off (or reduced) over several time periods. If the business will stay operational in the foreseeable future, the company can continue to recognize these long-term expenses over several time periods. Some red flags that a business may no longer be a going concern are defaults on loans or a sequence of losses. For example, Lynn Sanders purchases two cars; one is used for personal use only, and the other is used for business use only. According to the separate entity concept, Lynn may record the purchase of the car used by the company in the company’s accounting records, but not the car for personal use.

-

Document sans nom -

Search